by Dr Duncan Pickard

The governments of almost all countries have budget deficits and increasing national debts. The taxes* they currently collect are unable to meet the increasing costs of health and welfare provision for their older people and for the care and education of their young ones. Because the taxes they impose on earned incomes, employment and trade have severe negative effects on economic activity, the bases of the taxes are reduced, which means that different sources of revenue are needed.

Heads of governments have signed up to international projects, initiated by the Organisation for European Co-operation and Development (OECD), to prevent multinational companies and rich individuals from avoiding and evading taxation by relocating their money to countries with very low levels of taxation. They see this as an easy way to obtain more revenue. Dwyer (1), in his essay Tax Dodging and the Coming Tax Wars has described the problems involved when trying to collect taxes from companies and individuals who move money from one country to another. He has emphasised the failure of politicians to see the futility of their plans.

International projects to “wage war on tax avoidance” are fundamentally flawed because they are illegitimate in International Law. Individual countries are able to enforce laws only within their territorial boundaries. No sovereign state must obey others and so can not be obliged to collect taxes on their behalf. Exhortations by politicians to the chief executives of multinational companies to ‘pay their fair share of taxes’ are correctly met with the response that they pay all the taxes that they are legally obliged to pay. It is the legal duty of the directors of companies to maximise the financial returns of their shareholders and to comply with that they have to minimise the amount of tax the companies pay using all legal avoidance measures which are allowed.

It should be obvious to experienced politicians that their reliance on tax systems which are outdated, over-complicated and are severely disadvantageous to employment and enterprise should be replaced by a system which is suitable for the purpose of obtaining all the funds for the essential functions of government.

Hoping for significant improvements from tinkering with tax systems which have a long history of failure is ludicrous. There are examples of countries where tax revenues are obtained in sufficient amounts without detrimental effects on economic activity and with little or no avoidance or evasion. They are Singapore (2) and Hong Kong (3) . They derive most of the money needed for government from the collection of ground rent. They have few natural resources, but they have no annual budget deficits and high levels of economic prosperity. The collection of ground rent for the necessary functions of government was proposed by Adam Smith in 1776 (4) and William Ogilvie in1781 (5). It was supported by David Ricardo (6) and John Stuart Mill (7), and the theory was refined by Henry George (8) in “Progress and Poverty” (1879). He called it the ‘Single Tax’. I shall refer to it as Annual Ground Rent (AGR) which includes the economic rent of natural resources such as the electromagnetic spectrum and mineral and fossil fuel deposits as well as the ground on which we stand.

Classical economists subscribe to the four tenets which a tax system should have, they are :

1. It should not hinder employment or trade and so reduce the total fund from which the tax or charge must be paid.

2. For fairness, the amount of tax or charge levied should be related to the ability to pay and for justice, earned incomes should not be taxed whilst unearned rental incomes are left untaxed.

3. A tax or charge should be cheaply and easily collected so that the costs of administration are as low as possible.

4. There should be no opportunity for avoidance or evasion. *The Oxford dictionary defines ‘Tax’ as ‘a contribution to state revenue compulsorily levied on individuals, property or businesses’.

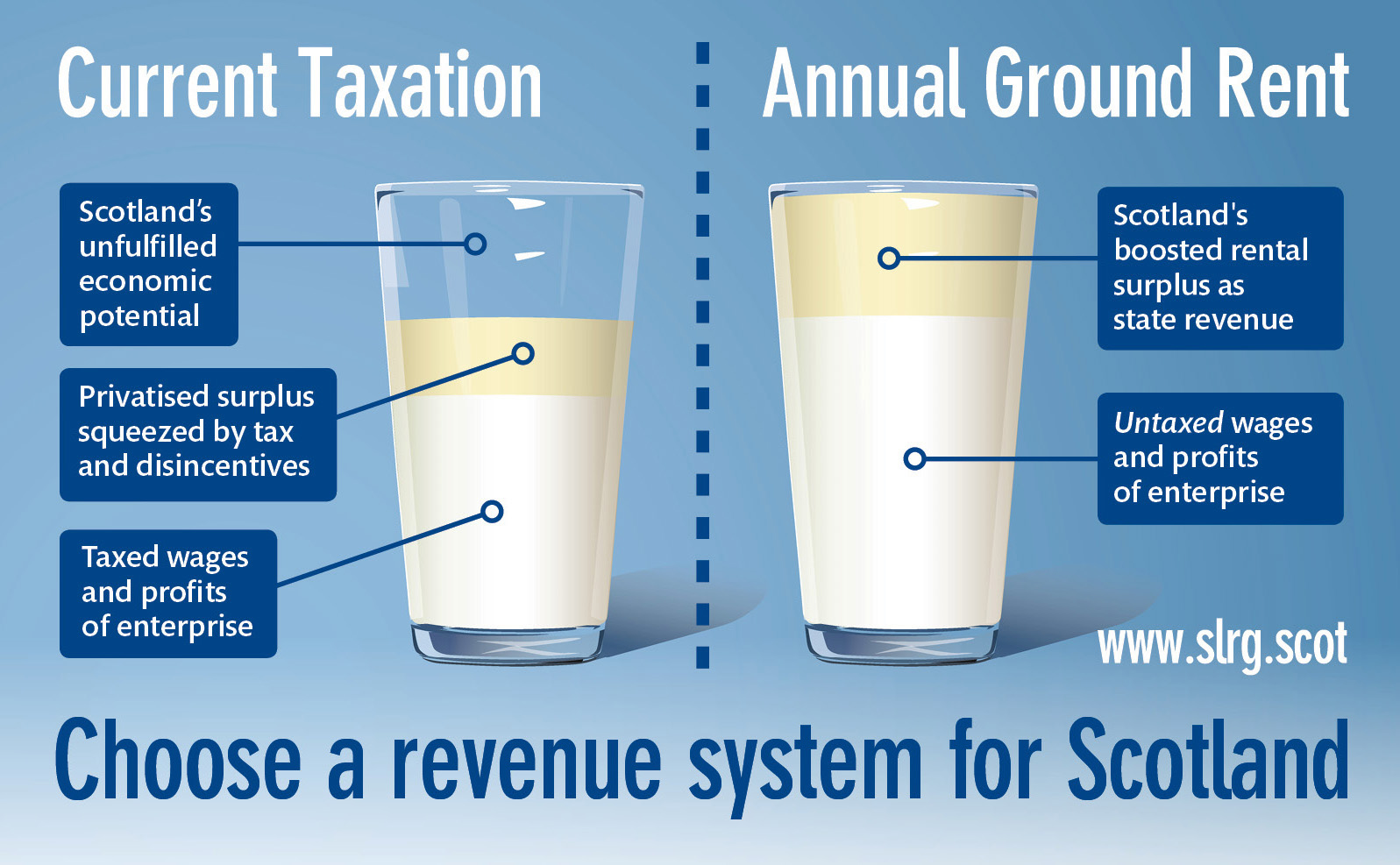

The collection of the Annual Ground Rent is the only fiscal charge which complies with these four tenets of taxation; most of the fiscal systems in use around the world fail miserably in comparison. An important feature of AGR is that it provides incentives to enterprise and trade by optimising the use of land. Almost all cities have areas of land which are derelict and disused; they contribute nothing to the creation of wealth and increase the cost of using other land whether to rent or buy, because they make useable land scarce.

A large area of land in the countryside is also unused or underused. By making an annual rental charge for occupying such land its owners would either make use of it or allow someone else to use it. Without the need for income taxes and sales taxes (such as VAT) employment and trade will increase and costs of production will fall (9). Those who advocate “wars on tax cheats” to collect more tax by international co-operation stand to be accused of behaving like a physician who repeatedly treats the symptoms of a disease and never looks for its cause or a cure. They opt for what they think is the easiest target without evaluating what is needed for the target to be hit or whether they have chosen the correct target. Instead of trying to raise more from existing taxes by trying to devise more effective ways of enforcement, they should be thinking of better methods of collecting the revenue they need.

The tenets of taxation listed above should be on display in every politician’s office. The economic case for the collection of the economic rent of every country to provide for its necessary functions is invincible. The reason why it is rarely used is due to the failure to overcome the claims of those with vested interests in retaining the status quo, who are usually a minority of the population but possess the loudest and most strident voices. The importance of gaining or retaining political power always over- rides plans for radical change.

Election manifestos contain vague promises of ‘fairness’, ‘justice’ and ‘working for the many, not the few’, with no commitments to the radical tax reforms which are needed. In Britain many years ago all the revenue for government was obtained from those who owned the land.(10) Gradually, taxation has been shifted onto the earnings of those who work, leaving most of the unearned rental value of the land to be collected by those who own it. It is not very long ago that ownership of land was a necessary qualification for having the right to vote or be eligible to be elected to parliament. The laws pertaining to the imposition of taxes were made by landowners.

Reference is often made to “The Law of the Land” which should be called “The Law of the Landowners”. The bias towards protecting the privileges of landowners has even been backed by the European Court of Human Rights. It declares the ‘right of everyone to the peaceful possession of his property’ but this only applies to a person’s existing possessions. It does not extend protection of property rights to include the right to property for everyone. Therefore it is not a universal human right. In the United Kingdom, a significant shift of the burden of taxation towards earned incomes and away from unearned incomes began about fifty years ago with the abolition of Schedule ‘A’ Property Tax whilst exemption from tax on mortgage interest was retained. The shift was accelerated twenty years later with greater emphasis on the ambition for a “Home – Owning Democracy”.

The government introduced the right of council house tenants to buy their homes at heavily discounted prices. Banks were allowed to provide mortgages for house purchase, a function which had been dominated by Building Societies whose lending capacity was limited by the amount of money which savers had deposited with them. This restrained rises in house prices. Their business model was based on the requirement for borrowers to have the ability to repay what they had borrowed. They were averse to taking risks and defaults were few.

Lending by banks was very different. Instead of close scrutiny of borrowers’ ability to repay, banks increasingly relied on the value of the collateral against which the mortgage was secured. So long as house prices were rising, the amount of money they were prepared to lend also rose. Banks were not restricted by the amount savers had on deposit because their fractional reserve facility allowed lending to rise with the demand for it. Residential property became the most profitable form of investment and many peoples’ net financial worth was gained more from the increase in the price of their houses, or more accurately, in the price of the land on which their houses stood, than from paid employment.

The preference of lenders for investment in landed property meant that those who wanted to invest in productive industry found it very difficult to obtain financial backing. The increase in the price of residential property is almost all untaxed, unearned income, a fact which is ignored by politicians and officials in the Treasury and the Bank of England. The high and rising price of houses is seen to be beneficial to the national economy because as more money is spent on houses, the higher is the GDP and the more politicians congratulate themselves on the success of their economic policy. The shortcomings of GDP as an index of economic prosperity are well known but the resistance to the adoption of a better index is formidable, from owners of residential property, the financial sector and politicians (11).

Nothing is produced by much of what is included in GDP. For instance, money which is spent on land does not produce more of it and money which is wasted on projects which fail, adds to GDP, as does the cost of repairing the damage caused by natural disasters although there is little net gain to the national wealth. A much better measure of economic prosperity is the amount of Annual Ground Rent in a country. One of the natural laws of economics states that as the population grows and production increases, the demand for land rises, which inevitably increases its economic rental value.

AGR is the surplus which remains from wealth production after labour and capital have received their just returns for their contribution to the production of wealth. All national governments should be obliged to collect the relevant statistics and publish the size of their AGR. They would then know the amount of revenue available to satisfy their necessary budgetary requirements, and could abolish all the harmful taxes which impede employment and trade, only retaining taxes on detrimental activities such as smoking and excessive alcohol consumption. It is accepted by most economists that countries should never aim to have an annual budget surplus. “That such a surplus would normally lead to a weak economy is obvious.

When the government has a surplus it is taking away from the purchasing power of its citizens more than it is adding back through its spending. Thus, it is contributing to a lack of demand”. (12) This statement needs to be challenged because it does not take account of the harmful effects on employment and trade of income taxes and general sales taxes. If government revenue is obtained from AGR and harmful taxes abolished, the resulting increase in wealth creation will produce sufficient growth in economic rent (AGR) for a budget surplus, which can be distributed as a national dividend and there will be no lack of demand. Politicians refuse to accept that they are responsible for recessions and the consequent damage to the lives of their citizens (13).

By wilfully ignoring the importance of speculative investment in land in the recurrence of booms and recessions, they persuade themselves that such events are inevitable and unpredictable. Instead of using their political power to prevent them, they react afterwards with stimulants, such as ‘Quantitative Easing’ to correct for ‘excessive exuberance’ or ‘market failure’. It is little wonder that the former governor of the Bank of England was unable to provide an adequate answer the Queen’s question, “Why did nobody see this (recession) coming”? All recessions are preceded by booms in landed property prices as speculative investors, encouraged by exemptions from taxation sanctioned by the government, bid prices up above what people can afford. A crash inevitably follows (14).

How have Singapore and Hong Kong managed to achieve the economic prosperity which has made them envied by others? Hong Kong was fortunate when the ‘ barren rock’ was leased from China in the nineteenth century because the ownership of the land remained with China and anyone who wanted to occupy land in Hong Kong had to lease it from the British colonial authority on the island. As the population grew and production increased, the prices bid for leases increased and the colonial authority used the money to fund the provision of basic services. The prosperity of Hong Kong had spectacular growth in the decade from 1961 under the supervision of its Financial Secretary, John Cowperthwaite. He refused to impose tariffs or give subsidies and he called his economic policy ‘positive non- intervention’ and said his job was to see that no economic harm was done. All the measures of social progress showed marked improvement, such as the rate of unemployment, literacy and the average age at death.

Singapore’s history of prosperity dates from the county’s achievement of independence in 1965. According to Phang Sock Yong of Singapore Management University, the city state flourished because its economic model contained ‘elements of (Henry) George’s land value capture. Singapore passed the Land Acquisition Act in 1966 which gave the state broad powers to acquire land.

In 1973, the concept of a statutory date was introduced, which fixed compensation values for land at the statutory date, November 30 1973. State land as a proportion of total land grew from 44% to 76% by 1985 and to about 90% in 2015. Rents that accrued from economic growth were invested in more and better infrastructure and taxes that damaged the economy were held down’. After adopting the radical reform I have described, the need for “a war on tax cheats” will disappear. Multinational companies which are involved in large increases in the production of wealth by their innovations and investments, automatically increase the amount of AGR, which currently adds to the price of landed property or disappears abroad.

With taxes on employment and trade abolished, unemployment will be minimised and wages will rise. All employers, including the multinational companies will be in competition for labour, and the enormous cost of welfare provision for the unemployed and underemployed will be greatly reduced. Governments will no longer need to persist in their futile attempts to impose taxes on the profits of corporations and the elusive money of rich individuals, most of whom make profits from expensive residential property on which they rarely pay tax.

References:

1. Dwyer,T. (2016) Tax dodging and the Coming Tax Wars, in Rent Unmasked, ed. Fred Harrison, Shepheard-Walwyn, London.

2. Sandilands, R. (2016) The Culture of Prosperity, in Rent Unmasked, ed. Fred Harrison, ShepheardWalwyn, London.

3. Purves, A. (2015) No Debt High Growth Low Tax, Shepheard-Walwyn, London

4. Smith, Adam (1776) The Wealth of Nations. Glasgow Edition, Oxford, 1976.

5. Ogilvie, William (1781) Essay on the Right to Property in Land, in Birthright in Land, Othilla Press, London, (1997).

6. Ricardo, D. (1818) Principles of Political Economy and Taxation, Prometheus Books, London. (1996).

7. Mill J.S. (1886) The Principles of Political Economy, Longmans, London.

8. George, Henry (1879) Progress and Poverty, Robert Schalkenbach Foundation, New York, (1979).

9. Gaffney, M. (2013) Europe’s Fatal Affair with Value Added Taxation, Groundswell, www.masongaffney.org

10. Harrison, Fred (2006) Ricrado’s Law, Shepheard-Walwyn, London.

11. Fiorentini, L. (2013) Gross Domestic Problem, Zed Books, London

12. Stiglitz, J. (2016) The Euro and its Threat to the Future of Europe, Allen Lane, London.

13. Harrison, Fred (2015) As Evil Does, Geophilos, London.

14. Harrison, Fred (2005) Boom Bust: House Prices, Banking and the Depression of 2010, ShepheardWalwyn, London.

Duncan Pickard BSc. PhD. Was a lecturer at the University of Leeds until 1990, he then took up farming full-time. He has farmed in Scotland since 1992 in partnership with his wife and two of their sons and their wives. They own 650 acres and farm another 1,000 acres on contract or on short-term leases. Dr. Pickard is the author of Lie of the Land (2004), Land Research Trust.