In the current tax regime land is permitted by society to be a private investment. Collecting AGR/LVT would partially or completely end this practice, which inflates land values far beyond their actual annual rental value (the amount someone would pay each year to monopolize a site’s natural and socially provided amenities.

When looking at the likely AGR liabilities it is therefore necessary to bear in mind that current site values are not a good guide. For example, prime farms today sell for about five times their productive value because governments choose to make them attractive investments with various tax breaks and access to subsidies.

This means that a proposed 1% AGR/LVT levy on prime agricultural land would not be £80 per acre (1% of today’s £8,000/acre) but £16 (1% of £1,600). A fundamental difference. And one which should also be borne in mind when predicting AGR liabilities for the owners of residential and urban sites.

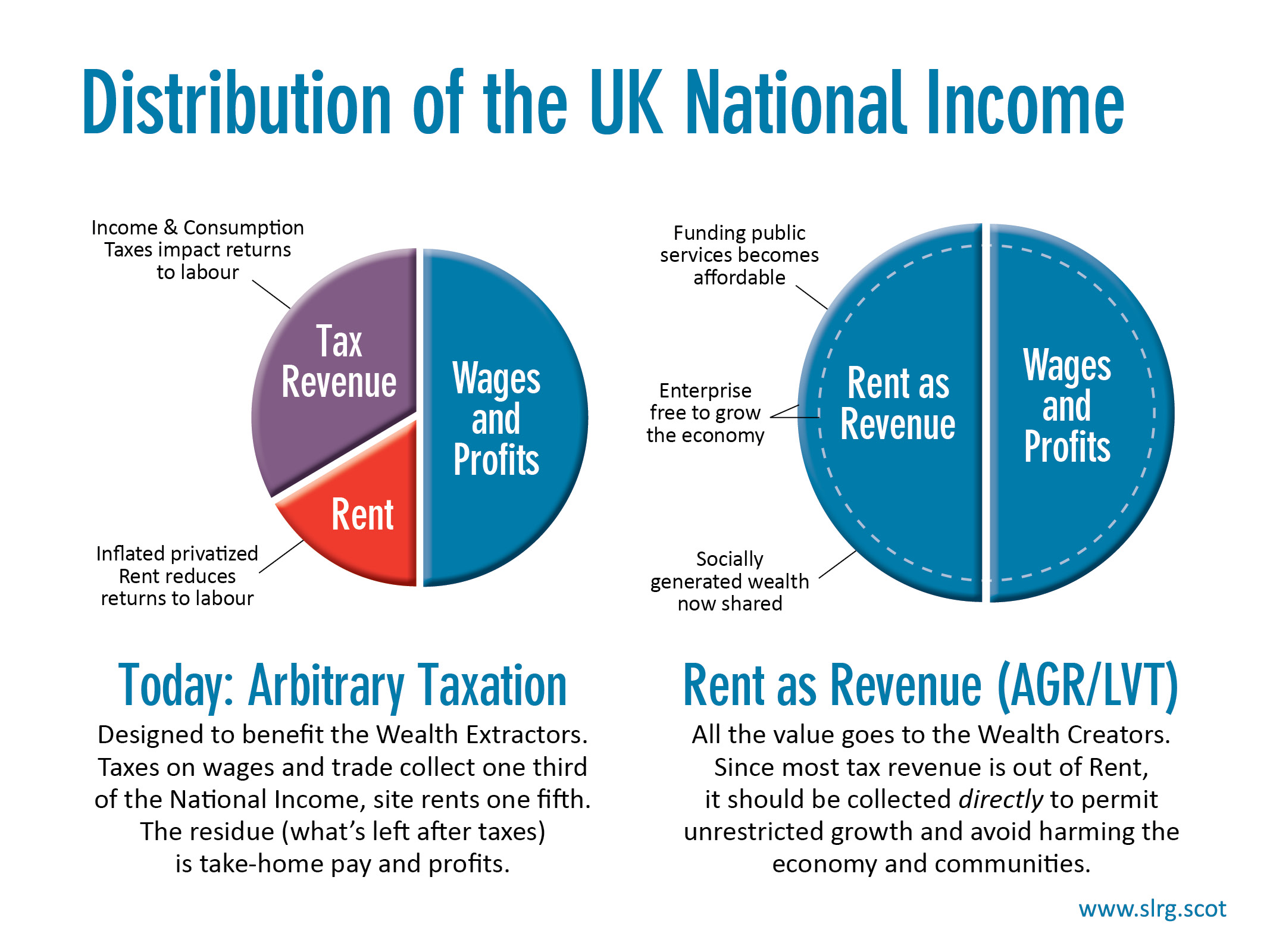

‘Economic Rent’ is the surplus wealth of a country which remains after the costs of labour and capital have been met. Most of it is pocketed as unearned income by those who own land.