The following documents are detailed PDF reports and will open in a new browser tab or window.

The burden of the economic crisis weighs heavily on the shoulders of society

AGR is a vast pool of income. It exceeds all current tax revenues put together, amounting to fully half of the UK gross national income. This resource – the product of society and nature – has been misappropriated for centuries, and, in the light of our failing economy, even prior to the pandemic, the time has come to redirect these 'returns' to the people who generate them. YOU!

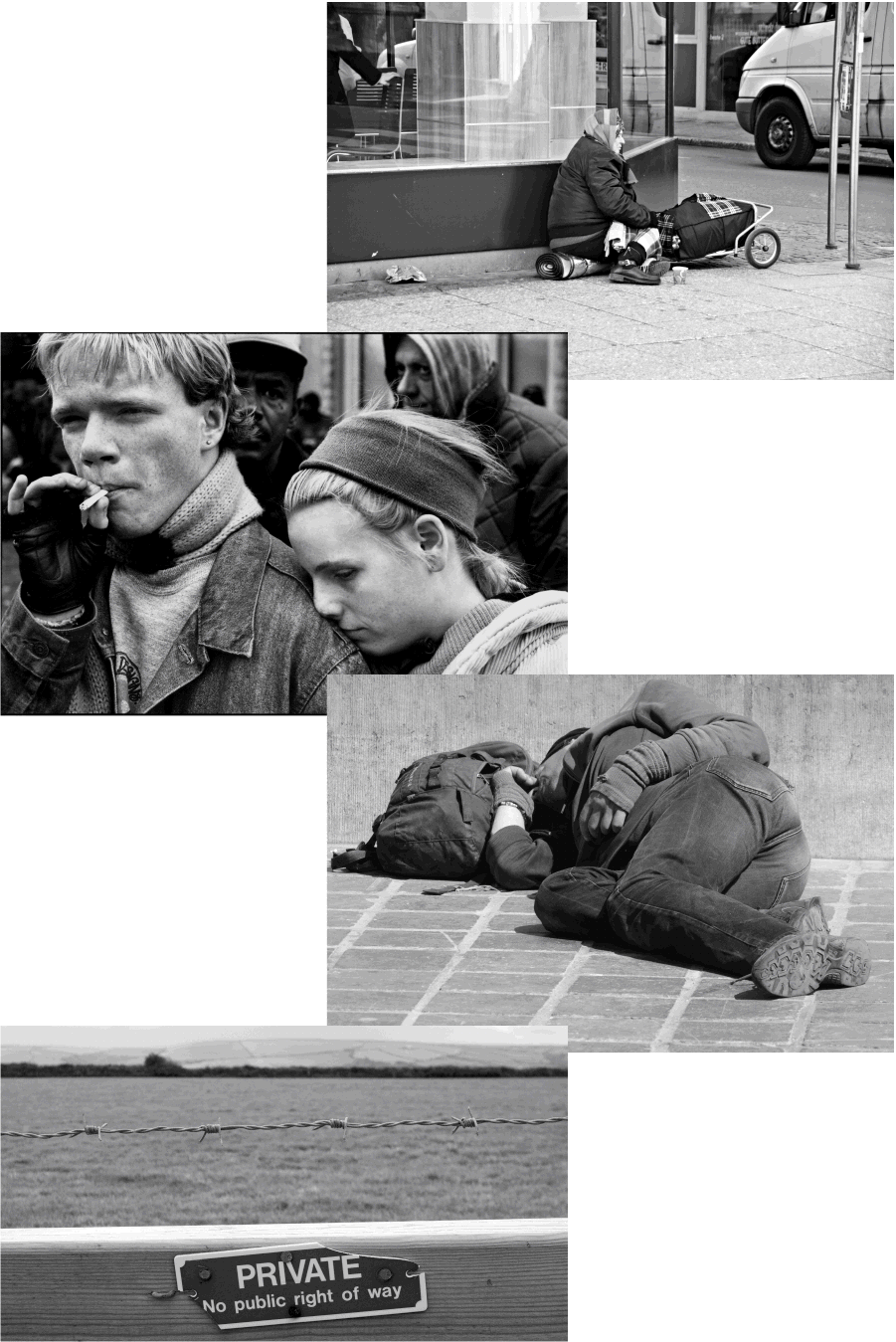

For over a year COVID has taken over our lives, obscuring the many problems that existed when things were so-called “normal”. We refer, of course, to rocketing food, fuel and rent costs; growing unemployment; spiralling homelessness and poverty; insufficient benefits for those in dire straits; escating mental health problems and drug deaths; and an alarming increase in reliance on food banks across the country.

For years, all of this has been 'addressed' by politicians of left, right and centre, with palliatives. Hiking up taxes, reducing benefits, restricting public service pay rises and spending, has entrenched inequality under the pretext of solving our problems. Meantime, no-one is doing anything to stop unregulated corporations hiking up prices, compounding the problems of an already struggling nation on the brink of a social and economic crisis.

Institutions that once served us, now rule us

Our existing economic system is unsustainable and divisive.

Powerful and faceless corporations are gaining more and more control through technology and entertainment.

The financial crisis should not become an excuse to raise taxes, which would only undermine the economic growth required to regain our strength. George W. Bush

These corporations make the rules, steer our choices and manipulate us so completely that we’re powerless to rebel.

Following the crash of 2008 society paid the price of reparation. Banks, the very cause of the problem, were bailed out and rewarded by money from the public purse. The country has not yet recovered and, according to our economists, another much worse crash is inevitable without AGR by 2026.

Robbing the poor to feed the rich!

"I am opposing a social order in which it is possible for one man who does absolutely nothing that is useful to amass a fortune of hundreds of millions of dollars, while millions of men and women who work all the days of their lives secure barely enough for a wretched existence". Eugene V. Debs

In the past, land was acquired by the nobility and became part of their capital assets, generating profit simply by virtue of ownership. Anyone using it – eg. a tenant - had to pay a premium in the form of "RENT".

This rent was not just for the property the tenant lived in, but also for the land the property stood on - which frequently doubled the cost and generating unearned financial returns (economic rent) for the landowner. This was a misappropriation of capital that was as much owed to the Community whose work and efforts generated the market value of the land.

This explains the success of the so-called "1%" (from owning rent-yielding assets), and the unearned windfalls accruing to UK homeowners today. But that "economic rent" is not just produced by its recipients; it is produced by, and therfore belongs to, EVERYONE!

"...We now condemn feudalism. We condemn not merely the feudal lords but we condemn the whole structure of rules that sustained feudalism. I am asking people to think similarly about the world economy". Thomas Pogge

The value of land then, was determined by society itself, through production and trade, as it still is today. So when society prospered and demand for amenities on the owners' land increased, the value of the land also increased. A landlord could then raise rents at will, without any improvements, and regardless of whether tenants could afford the increase or not. And since there were no regulations, and no system for people to complain, if tenants fell behind with their rent, they were evicted with no social support creating hunger, starvation, homelessness and poverty leading to the invention of the "workhouse".

Over time, even the common land which had fed and sustained much of the population, was 'enclosed' and removed from the publics’ right to free access. Universal access to land – required in order to survive – was now achieved either by owning it, or paying the owner. Is it any wonder we experience starved public services and a gulf between rich and poor that is at an all-time high?

Such were the tenets of feudalism that are still in practice today.

A future that benefits everyone

The dollar amount of the economic rent (AGR) flowing from natural resources is enormous, more than enough to fully fund the functions of government. The goal is to eliminate taxes on wages and trade in favor of collecting only the economic rent, much of which is currently being diverted to the owners of land and its natural resources). "Economic justice doesn't happen overnight, but by continually holding the vision of a fair system in mind we will eventually achieve our goal." Heather T. Remoff

ANNUAL GROUND RENT (AGR), also referred to as Land Value Tax (LVT), is based on the premise that free access of all land and everything in nature, is the birth right of every human being. AGR is a radical change to the unfair economic system that is crippling society and stifling enterprise, creativity and freedom.

Unlike other ‘taxes’ AGR does not raise money from labour or trade. Instead, Annual Ground Rent is a single payment charged on the ownership of land. Not just large estates and farms, but land beneath privately owned houses and businesses everywhere.

AGR is a vast pool of untapped income, exceeding all other tax revenues put together. In the light of our failing economy, even prior to the pandemic, the time has come to redirect the proceeds to the people who generate it. YOU.

AGR would be paid directly to the Government and distributed back into society via public services, which to date have been systematically eroded by the current economic system. Services such as the NHS, Educational Institutions and social support, public transport etc.

Following the introduction of the new AGR system, within a short period of time, rents would reduce by half or more and would be determined by the market value of bricks and mortar and improvements only.

“Our lives begin to end the day we become silent about things that matter... Change does not roll in on the wheels of inevitability, but comes through continuous struggle. And so we must straighten our backs and work for our freedom.” Martin Luther King

Initially, there are likely to be major objections from wealthy land-owners and even freehold property owners. But a closer look at the big picture of rapid growth, small and large business development, more money in everyone’s pockets, the eradication of homelessness and an end to gratuitous property speculation, would clearly demonstrate the benefits of this innovative system. And remember: everyone – including former land speculators – would receive a full fair share of their nation's net income (economic rent/AGR). There is no vengeance in AGR; just a future of growing shared prosperity.

ARG is the ONLY fiscal system that will create a fairer, more equal society. It is the ONLY logical response to society's SOS. The ONLY solution to breaking free from the destructive and corrosive financial claws that are gripping people's lives. The only solution that will restore and sustain personal independence, families, communities and democracy itself.